I wanted to replicate R's calculation on estimation of regression equation on below data:

set.seed(1)

Vec = rnorm(1000, 100, 3)

DF = data.frame(X1 = Vec[-1], X2 = Vec[-length(Vec)])

Below R reports estimates of coefficients

coef(lm(X1~X2, DF)) ### slope = -0.03871511

Then I manually estimate the regression estimate for slope

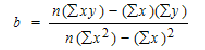

(sum(DF[,1]*DF[,2])*nrow(DF) - sum(DF[,1])*sum(DF[,2])) / (nrow(DF) * sum(DF[,1]^2) - (sum(DF[,1])^2)) ### -0.03871178

They are close but still are nor matching exactly.

Can you please help me to understand what am I missing here?

Any pointer will be very helpful.

CodePudding user response:

The problem is that X1 and X2 are switched in lm relative to the long formula.

Background

The formula for slope in lm(y ~ x) is the following where x and y each have length n and x is short for x[i] and y is short for y[i] and the summations are over i = 1, 2, ..., n.

Source of the problem

Thus the long formula in the question, also shown in (1) below, corresponds to lm(X2 ~ X1, DF) and not to lm(X1 ~ X2, DF). Either change the formula in the lm model as in (1) below or else change the long formula in the answer by replacing each occurrence of DF[, 1] in the denominator with DF[, 2] as in (2) below.

# (1)

coef(lm(X2 ~ X1, DF))[[2]]

## [1] -0.03871178

(sum(DF[,1]*DF[,2])*nrow(DF) - sum(DF[,1])*sum(DF[,2])) /

(nrow(DF) * sum(DF[,1]^2) - (sum(DF[,1])^2)) # as in question

## [1] -0.03871178

# (2)

coef(lm(X1 ~ X2, DF))[[2]] # as in question

## [1] -0.03871511

(sum(DF[,1]*DF[,2])*nrow(DF) - sum(DF[,1])*sum(DF[,2])) /

(nrow(DF) * sum(DF[,2]^2) - (sum(DF[,2])^2))

## [1] -0.03871511

CodePudding user response:

This is not a StackOverflow question per se, but rather a stats question for the sister site.

The narrow answer is that you can look into the R sources; it generally farms off to LAPACK and BLAS but a key part of the regression calculation is specialised in order to deal (in a statistically, rather than numerical way) with low-rank cases.

Anyway, here, I believe you are 'merely' not adjusting for degrees of freedom correctly which 'almost but not quite' washes out when you use 1000 observations. A simpler case follows, along with a 'simpler' way to calculate the coefficient 'by hand' which also has the advantage of matching:

> set.seed(1)

> Vec <- rnorm(5,100,3)

> DF <- data.frame(X1=Vec[-1], X2=Vec[-length(Vec)])

> coef(lm(X1 ~ X2, DF))[2]

X2

-0.322898

> cov(DF$X1, DF$X2) / var(DF$X2)

[1] -0.322898

>

CodePudding user response:

coef(lm(X1~X2, DF))

# (Intercept) X2

# 103.83714016 -0.03871511

You can apply the formula of coefficients in OLS matrix form as below.

X = cbind(1,DF[,2])

solve(t(X) %*% (X)) %*% t(X)%*% as.matrix(DF[,1])

giving,

# [,1]

#[1,] 103.83714016

#[2,] -0.03871511

which is same with lm() output.

Data:

set.seed(1)

Vec = rnorm(1000, 100, 3)

DF = data.frame(X1 = Vec[-1], X2 = Vec[-length(Vec)])