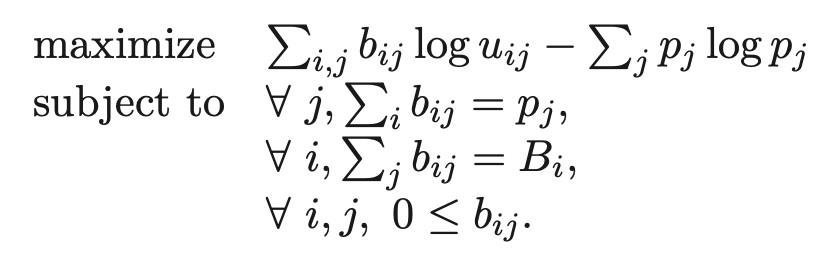

I want to solve the following convex optimization problem, where b is a matrix of variables and p is a vector of variables. The matrix u is a matrix of fixed non-negative values.

Here is my formulation in R, using the CVXR package. When I run it, SCS tells me that the status is unbounded. Am I formulating the problem incorrectly, or is this a bug in CVXR? Mathematically, it's easy to see that the objective function is bounded from above, so the problem cannot be unbounded.

R code

library(CVXR)

assemble_problem <- function(u, B) {

# Get size of problem, number of goods and bidders

m = nrow(u) # bidders

n = ncol(u) # goods

# Define variables

b <- Variable(m, n, name="spending", nonneg=TRUE)

p <- Variable(n, name="prices")

# Assemble objective

logu = apply(u, 1:2, log) # apply the log function to each entry in u

objective <- Maximize(sum(b*logu) sum(entr(p)))

# Assemble constraints

constraints <- list()

# Budget constraints

for (i in 1:m) { append(constraints, list(sum(b[i,]) == B[i])) }

# Spending constraints

for (j in 1:n) { append(constraints, list(sum(b[,j]) == p[j])) }

# Create and return problem

problem <- Problem(objective, constraints)

return(problem)

}

# Example

u <- matrix(c(1, 2, 3, 4), 2, 2)

B <- c(1, 1)

problem <- assemble_problem(u, B)

solution <- solve(problem, solver = "SCS", FEASTOL = 1e-4, RELTOL = 1e-3, verbose = TRUE)

# solution$status

Julia code

For completeness, I'm also attaching a Julia formulation (using Convex.jl) of the problem, which manages to solve the problem correctly.

using Convex, SCS

function assemble_problem(u, B)

# Get size of problem, number of bidders m and goods n

m, n = size(u)

# Define variables

b = Variable(m, n, Positive())

p = Variable(n)

# Assemble objective

logu = log.(u)

objective = sum(logu .* b) entropy(p)

# Assemble constraints

constraints = Constraint[]

# Budget constraints

for i in 1:m push!(constraints, sum(b[i,:]) == B[i]) end

# Price constraints

for j in 1:n push!(constraints, sum(b[:,j]) == p[j]) end

# Initialise and return problem

problem = maximize(objective, constraints)

return b, p, problem

end

u = [1 3; 2 4]

B = [1, 1]

b, p, prog = assemble_problem(u, B)

solve!(prog, () -> SCS.Optimizer())

CodePudding user response:

append in R does not work like push! in Julia. You have to assign the output:

# Budget constraints

for (i in 1:m) { constraints <- append(constraints, list(sum(b[i,]) == B[i])) }

# Spending constraints

for (j in 1:n) { constraints <- append(constraints, list(sum(b[,j]) == p[j])) }

Your list of constraints is empty otherwise.