I have a pandas dataframe with gaps in time series.

It looks like the following:

Example Input

--------------------------------------

Timestamp Close

2021-02-07 09:30:00 124.624

2021-02-07 09:31:00 124.617

2021-02-07 10:04:00 123.946

2021-02-07 16:00:00 123.300

2021-02-09 09:04:00 125.746

2021-02-09 09:05:00 125.646

2021-02-09 15:58:00 125.235

2021-02-09 15:59:00 126.987

2021-02-09 16:00:00 127.124

Desired Output

--------------------------------------------

Timestamp Close

2021-02-07 09:30:00 124.624

2021-02-07 09:31:00 124.617

2021-02-07 09:32:00 124.617

2021-02-07 09:33:00 124.617

'Insert a line for each minute up to the next available

timestamp with the Close value form the last available timestamp'

2021-02-07 10:03:00 124.617

2021-02-07 10:04:00 123.946

2021-02-07 16:00:00 123.300

'I dont want lines inserted here. As this date is not

present in the original dataset (could be a non trading

day so I dont want to fill this gap)'

2021-02-09 09:04:00 125.746

2021-02-09 09:05:00 125.646

2021-02-09 15:58:00 125.235

'Fill the gaps here again but only between 09:30 and 16:00 time'

2021-02-09 15:59:00 126.987

2021-02-09 16:00:00 127.124

What I have tried is:

'# set the index column'

df_process.set_index('Exchange DateTime', inplace=True)

'# resample and forward fill the gaps'

df_process_out = df_process.resample(rule='1T').ffill()

'# filter and return only timestamps between 09:30 and 16:00'

df_process_out = df_process_out.between_time(start_time='09:30:00', end_time='16:00:00')

However if I do it like this it also resamples and generates new timestamps on dates that are not existent in the original dataframe. In the example above it would also generate timestamps on a minute basis for 2021-02-08

How can I avoid this?

Furthermore is there a better way to avoid resampling over the whole time.

df_process_out = df_process.resample(rule='1T').ffill()

This generates timestamps from 00:00 to 24:00 and in the next line of code I have to filter most timestamps out again. Doesn't seem efficient.

Any help/guidance would be highly appreciated

Thanks

Edit:

As requested a small sample set

df_in: Input data

df_out_error: Wrong Output Data

df_out_OK: How the output data should look like

In the following ColabNotebook I prepeared a small sample.

Explanation

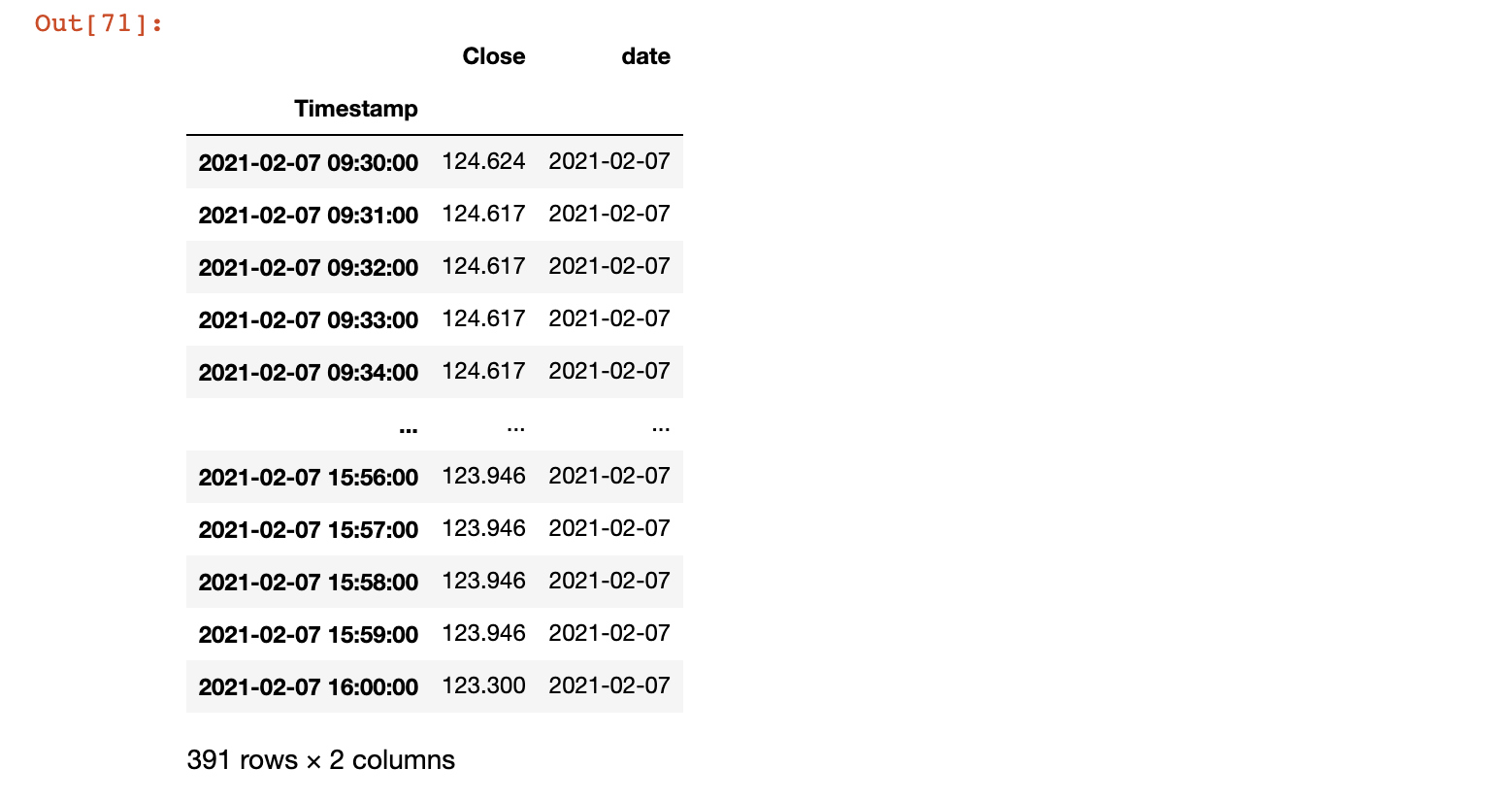

1. Resampling for limited time period only

"Furthermore is there a better way to avoid resampling over the whole time. This generates timestamps from 00:00 to 24:00 and in the next line of code I have to filter most timestamps out again. Doesn't seem efficient."

As in the above solution, you can resample and then ffill (or any other type of fill) using rule = 1Min. This ensures that you are not resampling from 00:00 to 24:00 but only from the start to end time stamps available in your data. To prove, I show this applied to a single date in the data -

#filtering for a single day

ddd = df[df['date']==df.date.unique()[0]]

#applying resampling on that given day

ddd.set_index('Timestamp').resample('1Min').ffill()

Notice the start (09:30:00) and end (16:00:00) timestamps for the given date.

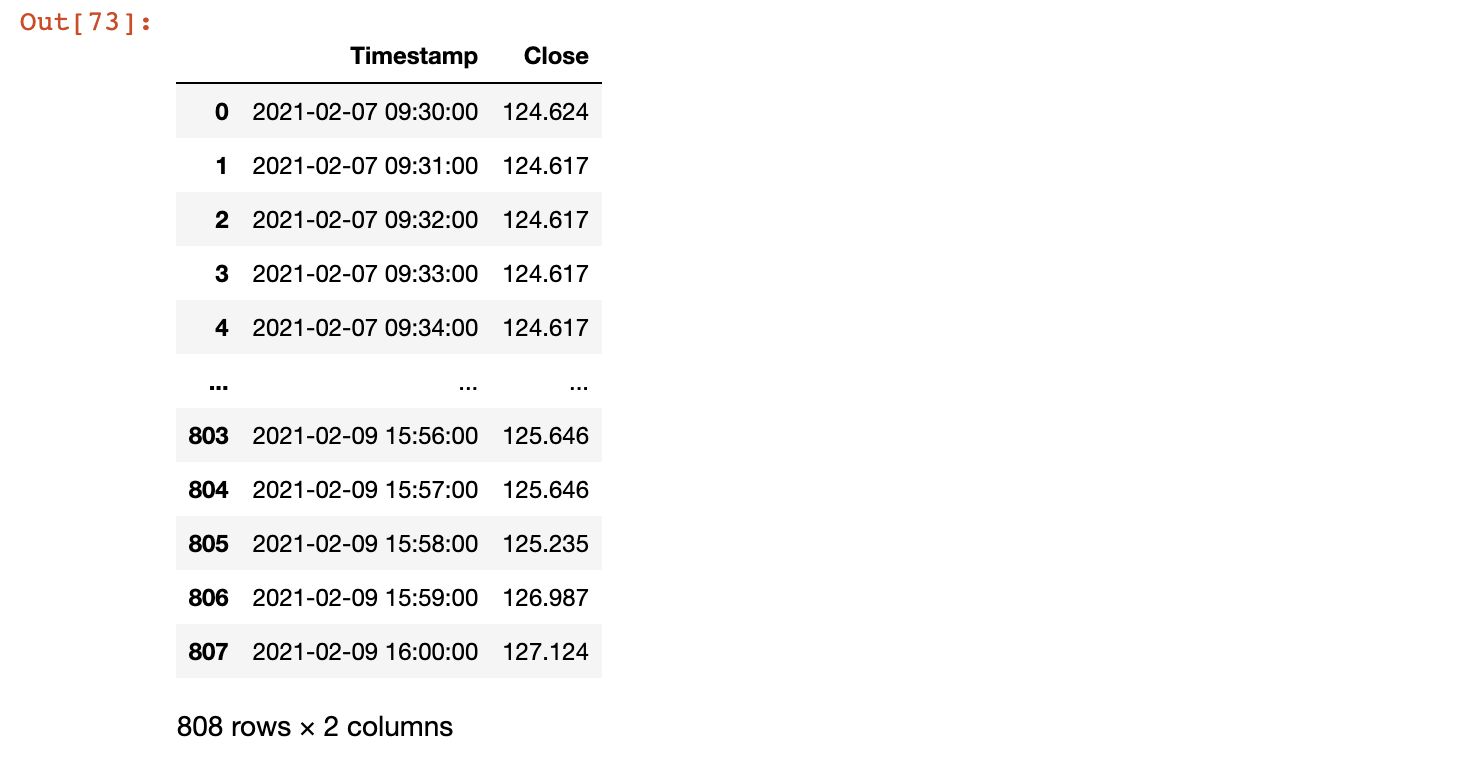

2. Applying resample over existing dates only

"In the example above it would also generate timestamps on a minute basis for 2021-02-08. How can I avoid this?"

As in the above solution, you can apply the resampling method over date groups separately. In this case, I apply the method using a lambda function after separating out the date from the timestamps. So the resample happens only for the date that exist in the dataset

df_new.Timestamp.dt.date.unique()

array([datetime.date(2021, 2, 7), datetime.date(2021, 2, 9)], dtype=object)

Notice, that the output only contains the 2 unique dates from the original dataset.