I have this R code for simulating log-return from Normal distribution. I have understood the code but lacking some knowledge to transform it to Julia fully.

R-Code

rt.sim<-rnorm(sim.size,mean=(mu_hat-s^2/2),sd=s)

Asset.sim<-rep(NA,sim.size)

Asset.sim[1]<-Asset[n]*exp(rt.sim[1])

for(i in 2:sim.size)Asset.sim[i]<-Asset.sim[i-1]*exp(rt.sim[i])

yl<-min(Asset)*0.85

yu<-max(Asset)*1.9

plot(ts(Asset),xlim=c(0,(n sim.size)),ylim=c(yl,yu))

lines((n 1):(n sim.size),Asset.sim,col="red",lwd=2)

grid(col="black",lwd=2)

This is my Julia version. I tried in this way and got error for this code. Can anyone help me to fix it? Julia Code

FTSE = df[!,"FTSE"]

Asset = FTSE

sim.size = 500 #got error here

n = length(Asset)

## log-return

rt = diff(log.(Asset))

rbar = mean(rt)

s = sd(rt)

delta_t = 1

mu_hat = rbar s^2/2

Random.seed!(123)

## Simulate log-return from Normal distribution

rt.sim = rand(Normal(s^2/2, s),sim.size)

Asset.sim = Vector{Int}(undef,sim.size)

Asset.sim[1] = Asset[n]*exp(rt.sim[1])

for i in 2:sim.size

Asset.sim[i] = Asset.sim[i-1]*exp(rt.sim[i])

end

yl = min(Asset)*0.85

yu = max(Asset)*1.9

plot(ts(Asset),xlim=c(0,(n sim.size)),ylim=c(yl,yu))

lines((n 1):(n sim.size),Asset.sim,col="red",lwd=2)

# grid(col="black",lwd=2)

CodePudding user response:

As Bogumil says in the main you need to move from using . in your variable names to _ or some other alternative.

The plot commands in your question aren't Julia syntax at all, here's a complete reproducible example:

using DataFrames, Distributions, MarketData, Plots, Statistics

# Get data from Yahoo

df = dropmissing(select(DataFrame(yahoo("^FTSE")), :timestamp, :AdjClose));

# Restricting range to have a similar number of observations to your plot

ftse = df.AdjClose[end-1900:end];

# Simulation dimensions

sim_size = 500;

n = length(ftse);

# Simulate log returns

log_return = diff(log.(ftse));

r̄ = mean(log_return);

σ = std(log_return);

μ̂ = r̄ σ^2/2;

rt_sim = rand(Normal(σ^2/2, σ), sim_size);

# More concise way of writing the loop

asset_sim = ftse[end] .* exp.(cumsum(rt_sim));

# Plot observed data and add simulated data to plot

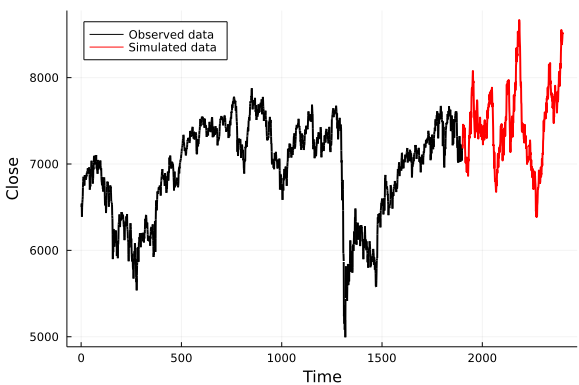

plot(ftse, color = "black", xlabel = "Time", ylabel = "Close", label = "Observed data", legend = :topleft)

plot!(n 1:n sim_size, asset_sim, color = "red", label = "Simulated data")

This gives:

(Clearly I've been using a different date range to yours. Also your simulation seems to have a stronger positive trend, note that in R you are using what looks like a volatility drag adjusted mean return, in the Julia version you create a μ̂ variable but are actually just using σ^2/2 as the mean return when drawing simulated returns)