Suppose I have an AR(3) simulated data, with an intercept of 3.

set.seed(247)

library(astsa)

sim1 = 3 arima.sim(list(order=c(3,0,0), ar=c(-0.1,-0.3,-0.5)), n=60)

pacf(sim1)

I can estimate the coefficients using:

est.1 = arima(x = sim1, order = c(3, 0, 0))

est.1

Coefficients:

ar1 ar2 ar3 intercept

-0.0614 -0.5098 -0.4286 2.9811

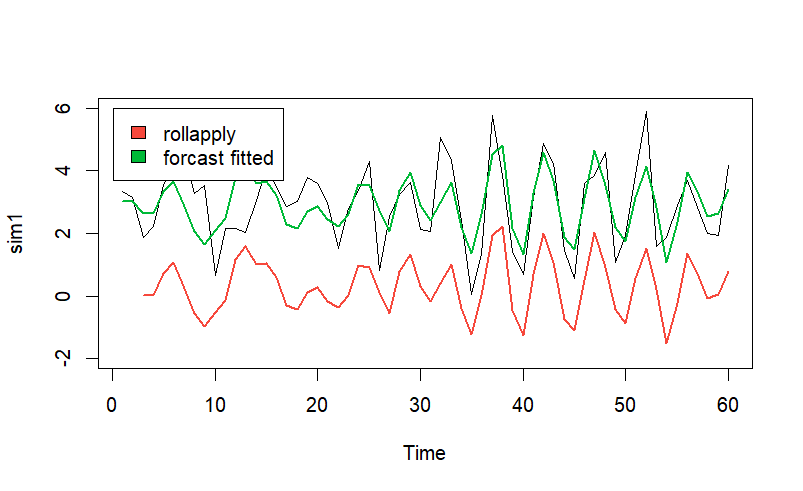

If I try to use rollapply of the zoo library, I get that the predictions are off-setted:

library(zoo)

library(forecast) # to compare

f1 = rollapply(zoo(sim1), 4, function(w) {sum(c(1,w[1:3])*rev(est.1$coef))},

align = "right", partial = T)

plot(sim1,type="l")

lines(f1, col = 2, lwd = 2) ## use the rollapply

lines(fitted(est.1), col = 3, lwd = 2) ## use the forecast package

legend(0.1, 6, legend=c("rollapply", "forcast fitted"), fill = c(2,3))

Can't figure out why it's happening...

CodePudding user response:

The model you are fitting is

y_t = 3 x_t

where

x_t = -0.1 x_{t-1} - 0.3 x_{t-2} - 0.5 x_{t-3} e_t.

This is equivalent to

y_t = 3*(1 0.1 0.3 0.5) - 0.1 y_{t-1} - 0.3 y_{t-2} - 0.5 y_{t-3} e_t

so the real "intercept" is 3*(1 0.1 0.3 0.5) = 5.7.