I would like to integrate a custom loss function for my LSTM in python. The code shows my approach so far. How would I best implement the loss function shown in the images? How would I handle the constraint <0?

Thanks for any help!

Code

# Importing the libraries

ep=25 #Epochs

bs=32 #Batch-Size

vs=0.2 #Validation-Split

r=ep 1 #Range

# Importing the training set

dataset_train = pd.read_csv(r'C:\Users\Name\Desktop\Recurrent Neural Networks\JPM_train.csv',delimiter =';')

training_set = dataset_train.iloc[:, 1:2].values

# Feature Scaling

from sklearn.preprocessing import MinMaxScaler

sc = MinMaxScaler(feature_range = (0, 1))

training_set_scaled = sc.fit_transform(training_set)

# Creating a data structure with 60 timesteps and 1 output

X_train = []

y_train = []

X_val=[]

y_val=[]

for i in range(60, 1516):

X_train.append(training_set_scaled[i-60:i, 0])

y_train.append(training_set_scaled[i, 0])

X_train, y_train, X_val, y_val = np.array(X_train), np.array(y_train), np.array(X_val), np.array(y_val)

# Reshaping

X_train = np.reshape(X_train, (X_train.shape[0], X_train.shape[1], 1))

# Importing the Keras libraries and packages

from keras.models import Sequential

from keras.layers import Dense

from keras.layers import LSTM

from keras.layers import Dropout

def custom_loss(y_true, y_pred):

if(#HERE):

loss=(predicted_stock_price-real_stock_price)^2

else:

loss=0

return loss

# Initialising the RNN

model = Sequential()

# Adding the first LSTM layer and some Dropout regularisation

model.add(LSTM(units = 50, return_sequences = True, input_shape = (X_train.shape[1], 1)))

model.add(Dropout(0.2))

# Adding a second LSTM layer and some Dropout regularisation

model.add(LSTM(units = 50, return_sequences = True))

model.add(Dropout(0.2))

# Adding a third LSTM layer and some Dropout regularisation

model.add(LSTM(units = 50, return_sequences = True))

model.add(Dropout(0.2))

# Adding a fourth LSTM layer and some Dropout regularisation

model.add(LSTM(units = 50))

model.add(Dropout(0.2))

# Adding the output layer

model.add(Dense(units = 1))

# Compiling the RNN

model.compile(optimizer = 'adam', loss = custom_loss ,metrics=['accuracy'])

# Fitting the RNN to the Training set

history=model.fit(X_train, y_train, epochs = ep, batch_size = bs, validation_split=vs)

# Getting the real stock price of 2017

dataset_test = pd.read_csv(r'C:\Users\Name\Desktop\Recurrent Neural Networks\JPM_test.csv',delimiter =';')

real_stock_price = dataset_test.iloc[:, 1:2].values

dataset_total = pd.concat((dataset_train['Preis'], dataset_test['Preis']), axis = 0)

inputs = dataset_total[len(dataset_total) - len(dataset_test) - 60:].values

inputs = inputs.reshape(-1,1)

inputs = sc.transform(inputs)

X_test = []

for i in range(60, 80):

X_test.append(inputs[i-60:i, 0])

X_test = np.array(X_test)

X_test = np.reshape(X_test, (X_test.shape[0], X_test.shape[1], 1))

predicted_stock_price = model.predict(X_test)

predicted_stock_price = sc.inverse_transform(predicted_stock_price)

history_dict = history.history

print(history_dict.keys())

accuracy = history_dict['accuracy']

validation_accuracy = history_dict['val_accuracy']

loss = history_dict['loss']

validation_loss = history_dict['val_loss']

gs = gridspec.GridSpec(2, 2)

#plt.tight_layout()

#plt.subplots_adjust(hspace=1.0)

fig = plt.figure(figsize=(16,16))

# Visualising the results

ax = plt.subplot(gs[1, :]) # row 1, span all columns

plt.plot(real_stock_price, color = 'red', label = 'Real Google Stock Price')

plt.plot(predicted_stock_price, color = 'blue', label = 'Predicted Google Stock Price')

plt.title('Google Stock Price Prediction')

plt.xlabel('Time')

plt.ylabel('Google Stock Price')

plt.legend()

plt.show()

Only the Custom loss function

def custom_loss(y_true, y_pred):

if(#HERE):

loss=(predicted_stock_price-real_stock_price)^2

else:

loss=0

return loss

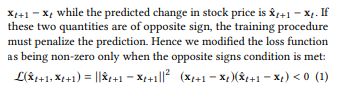

Pictures of the targeted loss function

Here is the link to the original text: https://www.researchgate.net/publication/342094242_Deep_Stock_Predictions

CodePudding user response:

You can use this loss function that calculates the current prediction (t1) minus the previous real_stock_price (t-1) :

def custom_loss(y_true, y_pred):

if((y_true[0]-y_true[1])*(y_pred-y_true[1])):

loss=(y_pred -y_true[0] )^2

else:

loss=0

return loss

I think that the derivatives in the backpropagation will not be affected by this shifting of time.