I am trying to build a basic Shiny App. I have the following fixed variables and a function.

################################

# Fixed variables

mtsSqrd = 10000

rent = 20 # per square foot

# Variables & Assumptions

# in mts squared

operatingExpensesPerc = 10

# general vacancy

vacancy = 0.10

purchasePrice = 1000000

capRate = 0.08

growthRateInc = 0.03

growthRateExp = 0.02

leveragedCapRateTableFunction = function(purchasePrice, capRate, equity){

####################################################

# First year

generalPotentialRev = mtsSqrd * rent

generalVacancy = generalPotentialRev * vacancy

effGrossRev = generalPotentialRev - generalVacancy

operatingExpenses = mtsSqrd * operatingExpensesPerc

netOpInc = effGrossRev - operatingExpenses

# Subsequent years

T = 5

generalPotentialRev_T = generalPotentialRev*(1 growthRateInc)^(1:T)

generalVacancy_T = generalPotentialRev_T * vacancy # we assume the vacancy rate is fixed over the years

effGrossRev_T = generalPotentialRev_T - generalVacancy_T

operatingExpenses_T = operatingExpenses*(1 growthRateExp)^(1:T)

netOpInc_T = effGrossRev_T - operatingExpenses_T

# Valuation at Sale

# NOI at year 6

salePrice = netOpInc_T[T] / capRate

####################################################

#loanToValuePerc = loanToValue

#loanToValue = purchasePrice * loanToValuePerc

#equity = purchasePrice - loanToValue

loanToValue = purchasePrice - equity

interestRate = 0.06

amortisationPeriod = 25 # years

interestRate_monthly = interestRate/12

amortisationPeriod_monthly = amortisationPeriod*12

years = 30

months = years*12

payment = FinCal::pmt(r = interestRate_monthly, n = amortisationPeriod_monthly, pv = loanToValue, fv = 0)

amortTable = FinancialMath::amort.table(Loan = loanToValue, pmt = payment*-1, i = 0.06, ic = 12, pf = 12, plot = FALSE)

amortSchedule = amortTable$Schedule %>%

data.frame() %>%

mutate(

year = rep(1:amortisationPeriod, each = 12)

)

amortScheduleCalcs = amortSchedule %>%

group_by(year) %>%

summarise(

sumInterestPaid = sum(Interest.Paid),

sumPrincipal = sum(Principal.Paid)

) %>%

mutate(

monthlyPayments = sumInterestPaid/12,

#monthlyPrincipal = sumPrincipal/12

InterestPrincipal = sumInterestPaid sumPrincipal,

monthlyInterestPrincipal = InterestPrincipal /12

)

cashFlows = bind_cols(

amortScheduleCalcs[1:6, ],

netOpInc = c(netOpInc, netOpInc_T)

) %>%

mutate(

cashFlowAfterDebtService = netOpInc - InterestPrincipal

)

NOI_Year_6 = cashFlows$netOpInc[6]

mortgageBalanceEOY_5 = amortSchedule$Balance[60]

netSaleProceeds = salePrice - mortgageBalanceEOY_5

# Leveraged returns

cashFlowStreamsLeveraged = c(equity*-1, cashFlows$cashFlowAfterDebtService[1:T-1], cashFlows$cashFlowAfterDebtService[T] netSaleProceeds)

internalRateOfRetrunLeveraged = jrvFinance::irr(cashFlowStreamsLeveraged)

return(internalRateOfRetrunLeveraged)

}

Running the function I can compute the following:

leveragedCapRateTableFunction(purchasePrice = 1000000, equity = 200000, capRate = 0.08)

[1] 0.2908751

However, I want to expand the function over to different combinations/scenarios of the capRate and purchasePrice. (Keeping the equity variable fixed.

In R I can define a new perc increase / decrease function and use expand grid to create the different combinations

percDecreaseIncreaseFunction = function(x, perc = perc, decrease = TRUE){

if(decrease == TRUE){

out = x (x * - perc)

} else {

out = x (x * perc)

}

return(out)

}

unleveragedCapRates = expand_grid(

propertyPrices = c(percDecreaseIncreaseFunction(purchasePrice, 0.10, FALSE),

percDecreaseIncreaseFunction(purchasePrice, 0.05, FALSE),

purchasePrice,

percDecreaseIncreaseFunction(purchasePrice, 0.05, TRUE),

percDecreaseIncreaseFunction(purchasePrice, 0.10, TRUE)),

capRates = c(

percDecreaseIncreaseFunction(capRate, 0.10, FALSE),

percDecreaseIncreaseFunction(capRate, 0.05, FALSE),

capRate,

percDecreaseIncreaseFunction(capRate, 0.05, TRUE),

percDecreaseIncreaseFunction(capRate, 0.10, TRUE)

))

However, when I try to use pmap I

- can't get it to work in R.

pmap(list( ...1 = leveragedCapRates$propertyPrices, ...2 = leveragedCapRates$capRates, ...3 = equity, ), ~leveragedCapRateTableFunction(..1, ..2, ..3) ) unlist() %>% matrix(ncol = 5, byrow = FALSE) %>% data.frame() %>% set_names(unique(leveragedCapRates$propertyPrices)) %>% add_column(capRates = unique(leveragedCapRates$capRates)) %>% relocate(capRates, everything()) %>% round(4)

- How can I pass an

input$equitywhen I pass it through aneventReactive()?

In the following App.R - I am having difficulty at the following point in the eventReactive() part of the server function.

pmap(list(

...1 = unleveredInputs()$propertyPrices,

...2 = unleveredInputs()$capRates,

...3 = input$equity,

),

~leveragedCapRateTableFunction(..1, ..2, ..3)

The output should be a 5 x 5 matrix looking something like (but not the same numbers)

Code / App.R

library(tidyverse)

library(shiny)

library(shinyWidgets)

################################

# Fixed variables

mtsSqrd = 10000

rent = 20 # per square foot

# Variables & Assumptions

# in mts squared

operatingExpensesPerc = 10

# general vacancy

vacancy = 0.10

purchasePrice = 1000000

capRate = 0.08

growthRateInc = 0.03

growthRateExp = 0.02

#leveragedCapRateTableFunction(purchasePrice = 1000000, equity = 200000, capRate = 0.08)

leveragedCapRateTableFunction = function(purchasePrice, capRate, equity){

####################################################

# First year

generalPotentialRev = mtsSqrd * rent

generalVacancy = generalPotentialRev * vacancy

effGrossRev = generalPotentialRev - generalVacancy

operatingExpenses = mtsSqrd * operatingExpensesPerc

netOpInc = effGrossRev - operatingExpenses

# Subsequent years

T = 5

generalPotentialRev_T = generalPotentialRev*(1 growthRateInc)^(1:T)

generalVacancy_T = generalPotentialRev_T * vacancy # we assume the vacancy rate is fixed over the years

effGrossRev_T = generalPotentialRev_T - generalVacancy_T

operatingExpenses_T = operatingExpenses*(1 growthRateExp)^(1:T)

netOpInc_T = effGrossRev_T - operatingExpenses_T

# Valuation at Sale

# NOI at year 6

salePrice = netOpInc_T[T] / capRate

####################################################

#loanToValuePerc = loanToValue

#loanToValue = purchasePrice * loanToValuePerc

#equity = purchasePrice - loanToValue

loanToValue = purchasePrice - equity

interestRate = 0.06

amortisationPeriod = 25 # years

interestRate_monthly = interestRate/12

amortisationPeriod_monthly = amortisationPeriod*12

years = 30

months = years*12

payment = FinCal::pmt(r = interestRate_monthly, n = amortisationPeriod_monthly, pv = loanToValue, fv = 0)

amortTable = FinancialMath::amort.table(Loan = loanToValue, pmt = payment*-1, i = 0.06, ic = 12, pf = 12, plot = FALSE)

amortSchedule = amortTable$Schedule %>%

data.frame() %>%

mutate(

year = rep(1:amortisationPeriod, each = 12)

)

amortScheduleCalcs = amortSchedule %>%

group_by(year) %>%

summarise(

sumInterestPaid = sum(Interest.Paid),

sumPrincipal = sum(Principal.Paid)

) %>%

mutate(

monthlyPayments = sumInterestPaid/12,

#monthlyPrincipal = sumPrincipal/12

InterestPrincipal = sumInterestPaid sumPrincipal,

monthlyInterestPrincipal = InterestPrincipal /12

)

cashFlows = bind_cols(

amortScheduleCalcs[1:6, ],

netOpInc = c(netOpInc, netOpInc_T)

) %>%

mutate(

cashFlowAfterDebtService = netOpInc - InterestPrincipal

)

NOI_Year_6 = cashFlows$netOpInc[6]

mortgageBalanceEOY_5 = amortSchedule$Balance[60]

netSaleProceeds = salePrice - mortgageBalanceEOY_5

# Leveraged returns

cashFlowStreamsLeveraged = c(equity*-1, cashFlows$cashFlowAfterDebtService[1:T-1], cashFlows$cashFlowAfterDebtService[T] netSaleProceeds)

internalRateOfRetrunLeveraged = jrvFinance::irr(cashFlowStreamsLeveraged)

return(internalRateOfRetrunLeveraged)

}

percDecreaseIncreaseFunction = function(x, perc = perc, decrease = TRUE){

if(decrease == TRUE){

out = x (x * - perc)

} else {

out = x (x * perc)

}

return(out)

}

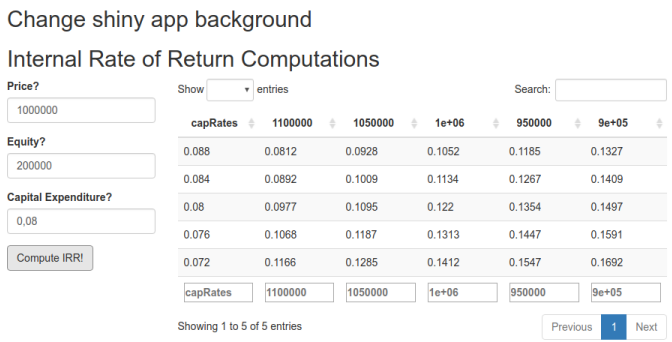

ui <- fluidPage(

tags$h2("Change shiny app background"),

setBackgroundColor("white"),

# Application title

titlePanel("Internal Rate of Return Computations"),

fluidRow(

column(3,

numericInput("purchasePrice", label = "Price?", value = 1000000, min = 1),

numericInput("equity", label = "Equity?", value = 200000, min = 1), # the max should be dependent on the max of the purchasePrice input

numericInput("capRate", label = "Capital Expenditure?", value = 0.08, min = 0, max = 1, step = 0.01),

actionButton("computeIRR", "Compute IRR!")

),

column(9,

dataTableOutput(("leveredirrTable"))

)

)

)

################################################################################

server <- function(input, output) {

############ Unlevereaged inputs #########################################

unleveredInputs <- eventReactive(input$computeIRR, {

expand_grid(

propertyPrices = c(

percDecreaseIncreaseFunction(x = input$purchasePrice, 0.10, FALSE),

percDecreaseIncreaseFunction(input$purchasePrice, 0.05, FALSE),

input$purchasePrice,

percDecreaseIncreaseFunction(input$purchasePrice, 0.05, TRUE),

percDecreaseIncreaseFunction(input$purchasePrice, 0.10, TRUE)

),

capRates = c(

percDecreaseIncreaseFunction(input$capRate, 0.10, FALSE),

percDecreaseIncreaseFunction(input$capRate, 0.05, FALSE),

input$capRate,

percDecreaseIncreaseFunction(input$capRate, 0.05, TRUE),

percDecreaseIncreaseFunction(input$capRate, 0.10, TRUE)

)

# equity = c(

# input$equity

# )

) %>%

data.frame()

})

leveredIRR <- eventReactive(unleveredInputs(), {

req(unleveredInputs())

pmap(list(

...1 = unleveredInputs()$propertyPrices,

...2 = unleveredInputs()$capRates,

...3 = input$equity,

),

~leveragedCapRateTableFunction(..1, ..2, ..3)

) %>%

unlist() %>%

matrix(ncol = 5, byrow = FALSE) %>%

data.frame() %>%

set_names(unique(unleveredInputs()$equity)) %>%

add_column(capRates = unique(unleveredInputs()$capRates)) %>%

relocate(capRates, everything()) %>%

round(4)

})

output$leveredirrTable <- renderDataTable(leveredIRR(), options = list(pageLength = 5))

observeEvent(unleveredInputs(), {

print(leveredIRR())

})

}

shinyApp(ui = ui, server = server)

CodePudding user response:

Try this

server <- function(input, output, session) {

############ Unlevereaged inputs #########################################

unleveredInputs <- eventReactive(input$computeIRR, {

expand_grid(

propertyPrices = c(

percDecreaseIncreaseFunction(x = input$purchasePrice, 0.10, FALSE),

percDecreaseIncreaseFunction(input$purchasePrice, 0.05, FALSE),

input$purchasePrice,

percDecreaseIncreaseFunction(input$purchasePrice, 0.05, TRUE),

percDecreaseIncreaseFunction(input$purchasePrice, 0.10, TRUE)

),

capRates = c(

percDecreaseIncreaseFunction(input$capRate, 0.10, FALSE),

percDecreaseIncreaseFunction(input$capRate, 0.05, FALSE),

input$capRate,

percDecreaseIncreaseFunction(input$capRate, 0.05, TRUE),

percDecreaseIncreaseFunction(input$capRate, 0.10, TRUE)

)

, equity = c(

input$equity

)

) %>%

data.frame()

})

leveredIRR <- eventReactive(unleveredInputs(), {

req(unleveredInputs())

A = unleveredInputs()$propertyPrices

B = unleveredInputs()$capRates

C = input$equity

vars <- list(A, B, C)

pmap(vars, ~leveragedCapRateTableFunction(..1, ..2, ..3)

) %>%

unlist() %>%

matrix(ncol = 5, byrow = FALSE) %>%

data.frame() %>%

set_names(unique(unleveredInputs()$equity)) %>%

add_column(capRates = unique(unleveredInputs()$capRates)) %>%

relocate(capRates, everything()) %>%

round(4)

})

output$leveredirrTable <- renderDataTable(leveredIRR(), options = list(pageLength = 5))

observeEvent(unleveredInputs(), {

print(leveredIRR())

})

}