I have a outer/inner loop-based function I'm trying to vectorise using Python Polars DataFrames. The function is a type of moving average and will be used to filter time-series financial data. Here's the function:

def ma_j(df_src: pl.DataFrame, depth: float):

jrc04 = 0.0

jrc05 = 0.0

jrc06 = 0.0

jrc08 = 0.0

series = df_src['close']

for x in range(0, len(series)):

if x >= x - depth*2:

for k in np.arange(start=math.ceil(depth), stop=0, step=-1):

jrc04 = jrc04 abs(series[x-k] - series[x-(k 1)])

jrc05 = jrc05 (depth k) * abs(series[x-k] - series[x-(k 1)])

jrc06 = jrc06 series[x-(k 1)]

else:

jrc03 = abs(series - (series[1]))

jrc13 = abs(series[x-depth] - series[x - (depth 1)])

jrc04 = jrc04 - jrc13 jrc03

jrc05 = jrc05 - jrc04 jrc03 * depth

jrc06 = jrc06 - series[x - (depth 1)] series[x-1]

jrc08 = abs(depth * series[x] - jrc06)

if jrc05 == 0.0:

ma = 0.0

else:

ma = jrc08/jrc05

return ma

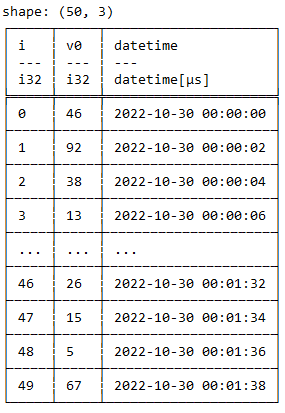

The tricky bit for me are multiple the inner loop look-backs (for k in...). I've looked through multiple examples that use groupby_dynamic on the timeseries data. For example,

...I can do a grouping by datetime like this":

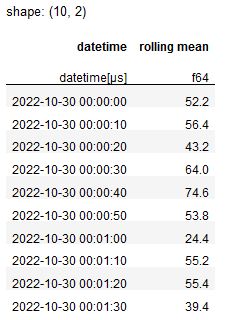

df.groupby_dynamic("datetime", every="10s").agg([

pl.col("v0").mean().alias('rolling mean')

])

which gives this:

But there's 3 issues with this:

- I don't want to group of datetime...I want to group on every row (maybe

i?) in bins of [x] size. - I need values against every row

- I would like to define the aggregation function, as per the various cases in the function above

Any tips on how I could attack this using Polars? Thanks.

CodePudding user response:

Are you searching for periods="10i"? Polars groupby_rolling accepts a period argument with the following query language:

- 1ns (1 nanosecond)

- 1us (1 microsecond)

- 1ms (1 millisecond)

- 1s (1 second)

- 1m (1 minute)

- 1h (1 hour)

- 1d (1 day)

- 1w (1 week)

- 1mo (1 calendar month)

- 1y (1 calendar year)

- 1i (1 index count)

Where i is simply the number of indices/rows.

So on your data a rolling groupby where we count the number of slots would give:

(df.groupby_rolling(index_column="i", period="10i")

.agg([

pl.count().alias("rolling_slots")

])

)

run GroupbyRollingExec

shape: (50, 2)

┌─────┬───────────────┐

│ i ┆ rolling_slots │

│ --- ┆ --- │

│ i64 ┆ u32 │

╞═════╪═══════════════╡

│ 0 ┆ 1 │

│ 1 ┆ 2 │

│ 2 ┆ 3 │

│ 3 ┆ 4 │

│ ... ┆ ... │

│ 46 ┆ 10 │

│ 47 ┆ 10 │

│ 48 ┆ 10 │

│ 49 ┆ 10 │

└─────┴───────────────┘

CodePudding user response:

def ma_j(df_src: pl.DataFrame, depth: float):

jrc04 = 0.0

jrc05 = 0.0

jrc06 = 0.0

jrc08 = 0.0

series = df_src['close']

for x in range(0, len(series)):

if x >= x - depth*2:

for k in np.arange(start=math.ceil(depth), stop=0, step=-1):

jrc04 = jrc04 abs(series[x-k] - series[x-(k 1)])

jrc05 = jrc05 (depth k) * abs(series[x-k] - series[x-(k 1)])

jrc06 = jrc06 series[x-(k 1)]

else:

jrc03 = abs(series - (series[1]))

jrc13 = abs(series[x-depth] - series[x - (depth 1)])

jrc04 = jrc04 - jrc13 jrc03

jrc05 = jrc05 - jrc04 jrc03 * depth

jrc06 = jrc06 - series[x - (depth 1)] series[x-1]

jrc08 = abs(depth * series[x] - jrc06)

if jrc05 == 0.0:

ma = 0.0

else:

ma = jrc08/jrc05

return ma